Visual Hive Blog

Your (Trade)-Show Sells Square Metres. The Market Pays More for Signal.

By Visual Hive

Published

8 min read

TLDR

Events businesses sell at ten to fifteen times earnings. Data businesses sell at nearly thirty. Informa proved the gap is real, in this industry, in one year.

But you do not capture it by carving off a data company and selling it. That is the move that sank dunnhumby. You capture it by folding owned, contextual data into the core, so the whole business re-rates, not a fragment you have to defend.

And in the AI era, data without context is worthless. The asset is meaning, not records.

You own an events business. You know what it is worth, near enough, because the whole industry trades in the same band. Ten to fifteen times earnings.

You have watched deals land in that range for years, so you model your own exit against it without much thought. It feels less like a number someone chose and more like a law of physics.

It is the smaller of the two numbers available to you. The gap between them is wider than almost anyone in the room realises.

The band everyone trades in

The band is right. Trade shows sit at the lower end of it, on thin barriers to entry and revenue that arrives once a year and has to be won all over again the next.

That is not a criticism of the work. It is how a buyer reads the cash flow: annual, transactional, re-earned every cycle. Worth a fair multiple, not a generous one.

So far none of this should surprise you. Hold it for a moment, because the next fact comes from inside the world you already know.

The same company. The same year. Nearly double.

Between 2022 and 2024, Informa, the largest exhibitions organiser in the world, sold its data and intelligence brands at a blended twenty-eight times earnings.

In the same window it bought events businesses at around ten. The market priced the whole group at roughly fifteen.

One company. One management team. It buys events at ten, trades at fifteen, sells data at twenty-eight.

The business did not change between those numbers. The only thing that moved the multiple was the shape of the revenue. So the distance between ten and twenty-eight is not the distance between a worse business and a better one. It is the distance between two ways of describing the same pound: won once, or recurring.

And here is the part that should sit with you. Every B2B show already produces the raw material of the higher number. Registrations. Ticket flows. Who walked where on the floor. The meetings booked, the sessions attended, who someone was last year and who they came back as this year.

Most of it is never unified, rarely owned in one place, almost never used. So it leaves the building as exhaust, and you price the business as though it were never there.

The move everyone reaches for

The move looks obvious, then. The market pays double for data. You have data. So you build a data product, carve it off, and sell it at twenty-eight, exactly as Informa did.

This is the conclusion nearly everyone reaches the moment they see the number. It is clean, it is precedented, and it is wrong.

There is a corpse attached to it.

The corpse attached to it

dunnhumby was the analytics engine behind Tesco’s Clubcard. A genuine data business, selling insight back to the brands that wanted to reach Tesco shoppers.

It was mooted for sale at up to roughly two billion pounds. Then a buyer examined it as a standalone asset, the bids collapsed toward seven hundred million, and the sale was scrapped.

The reason is the whole lesson. Held up to the light on its own, the value depended on a relationship and a set of contracts the seller did not fully control. More than half the revenue traced to a single client. Key terms could be unwound on a change of control.

The analytics were never the asset. The owned, contracted, defensible data was, and it was not as owned as it looked. So the asset was real right up until it was examined, and it was examined precisely because someone tried to sell it as a separate thing.

That is what the carve-out route does. It puts your data alone in the room, facing the most hostile examination in finance, with nothing to lean on.

A serious buyer runs that examination to do one thing: convert every claim into evidence, and discount whatever cannot be evidenced. Projected revenue with no signed contracts behind it gets stripped out and parked as “potential,” which is a polite word for “not paid for at close.”

So the obvious plan does not merely carry risk. It walks your most valuable, least provable asset straight into the one process built to disbelieve it.

What the twenty-eight actually teaches

Here is where I part company with the obvious reading of the Informa number.

Twenty-eight times is a wonderful multiple. But it was paid on the data portion only. A relatively small slice, spun out and sold on its own.

Nobody is going to value an entire events portfolio at twenty-eight, because the events are still events. So “carve off a data company and sell it high” is chasing a large multiple on a small number, while marching that small number into the dunnhumby examination. It is the trap dressed up as the prize.

The better move runs the other way, and it is quieter.

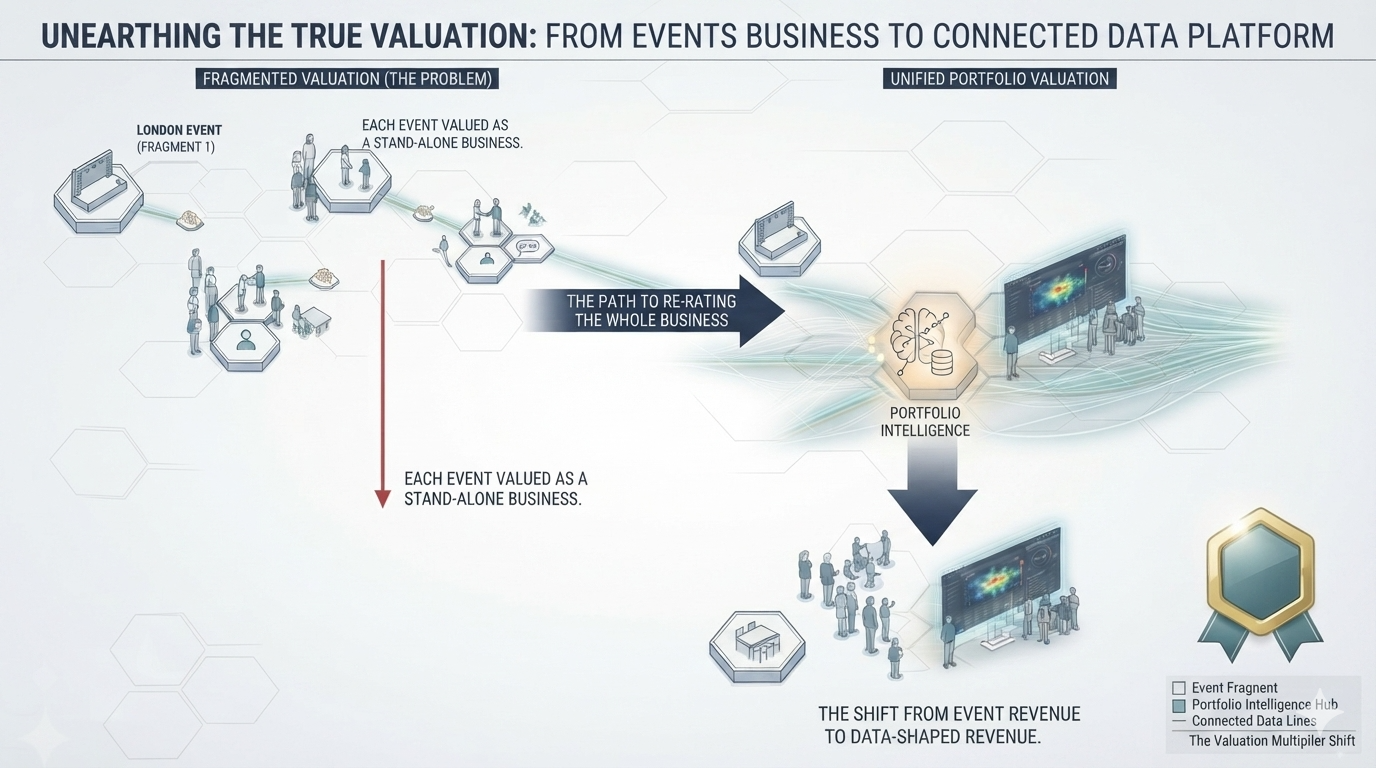

Do not build a data company to sell beside your events. Make your events themselves the data resource. Fold the unified, owned, provable data into the core business, so the show stops reading as square metres re-sold annually and starts reading as recurring, defensible, data-rich revenue.

You are not trying to win a big multiple on a small slice you have to amputate and then defend. You are trying to lift the multiple on the whole business. The large number.

So a modest re-rating across the entire portfolio is worth far more than twenty-eight times on a fragment, and it never has to survive being sold as a standalone asset, because it is not one. It is the quality of your core revenue, and quality of core revenue is the thing a buyer pays up for without a fight.

You get the event. They get the re-rate.

This is not theory built on one company. RELX, once a print publisher that also ran exhibitions, spent three decades rebuilding around information and analytics. It is now priced like an information business rather than a media one.

Tellingly, inside that group, the events division is the lower-multiple part. The pattern holds wherever it shows up: a data layer on top of an operating business re-rates the whole thing, not a fragment of it.

But a re-rate built on recurring data revenue only holds if that revenue is durable, and durable means defensible. That is the one thing the AI era has quietly taken off the table for generic data. More on that in a moment.

The re-rate also only lands with you if the data is yours. The personalised email, the recommendation engine, the smart matchmaking all lift your show whoever runs them. So if the unified data beneath them lives inside someone else’s platform, the durable asset sits with that vendor.

You get the event. They get the re-rate.

The only question worth your time

So the question is not “do I have data.” Every show has data.

And in 2026 that sentence is worth less than it has ever been, because foundation models have made generic, scrapeable data close to free. If your data is the kind a model already holds, or a rival could assemble, it is a commodity. A commodity earns no premium, and sustains no subscription anyone keeps paying for.

So the buyer’s real test has two layers, and the AI era has flipped which one matters most.

The first one used to come second. Is the data the kind that still means anything? Continuously refreshed, behavioural, first-party, and above all contextual.

Does it produce the one signal a generic tool cannot: the gap between what someone declares and what they actually do? The visitor who ticks “just browsing” at registration, then spends the day at three competitors’ stands.

The badge scans are data. Knowing what that contradiction means is context. Catching it needs both the unified record of the behaviour and a read on what the behaviour means, which is exactly what a pile of raw exhaust, or a model fed that exhaust, cannot give you.

Owning a pile of records is not owning an asset.

Only if the data clears that test does the second layer matter, the one a buyer will still run whether you have prepared for it or not. Could you prove you own it, in a room full of someone else’s lawyers?

That it is unified, not scattered across a registration system, a badge scanner, an app and a sponsor dashboard that never speak. That you own it rather than rent it from a vendor whose platform it actually lives in. That you hold the right to aggregate it, anonymise it and use it, the precise right dunnhumby turned out to lack.

Because owning a commodity, provably, even on a subscription, still earns you nothing. The thing that re-rates the business is data that carries meaning, that no one else can assemble, refreshed with every event. That is the asset. The records were only ever the raw material.

If you have that, your core business re-rates, quietly, across the whole portfolio. If what you have is a pile of records you could prove you own but could not say what they mean, the AI era has already priced it for you. The show stays priced as square metres.

The piece of infrastructure that turns scattered event exhaust into data that actually means something, owned and provable and ready the moment a product needs it, is a specific thing. What it is, how the unification works, and why owning that layer is the whole game, is the next piece.

For now, only one question is worth your time, and it is worth asking before a buyer asks it for you. Not “how good is our show.” You know the answer to that.

The one almost nobody asks until the term sheet is on the table: are we an events business sitting on data we have never made mean anything, or a data-rich business the market has simply not been forced to re-rate yet?

There is no one recipe for this. But there is a solution, and we have built it.

The next piece lands in two weeks. If you want to talk before then, get in touch.

This piece draws on a research briefing prepared by Allenby Advisory and Visual Hive on data and enterprise value in B2B events. Valuation figures are point-in-time and drawn from public company filings and named transactions; multiples move, and any number used here should be dated to its source.

Read this on LinkedIn